There are several uncertainties that arise when buyers and sellers across the globe engage in maritime trade operations. Some of these uncertainties revolve around delayed payments, slow deliveries, and financing-related issues, among others. The sheer distances involved in international trade, different laws and regulations, and changing political landscape are just some of the reasons for sellers needing a guarantee of payment when they deliver goods through the maritime route to their sellers. Letters of credit were introduced to address this by adding a third party like a financial institution into the transaction to mitigate credit risks for exporters.

What is a Letter of Credit?

A letter of credit or LC is a written document issued by the importer’s bank (opening bank) on importer’s behalf. Through its issuance, the exporter is assured that the issuing bank will make a payment to the exporter for the international trade conducted between both the parties.

The importer is the applicant of the LC, while the exporter is the beneficiary. In an LC, the issuing bank promises to pay the mentioned amount as per the agreed timeline and against specified documents.

A guiding principle of an LC is that the issuing bank will make the payment based solely on the documents presented, and they are not required to physically ensure the shipping of the goods. If the documents presented are in accord with the terms and conditions of the LC, the bank has no reason to deny the payment.

Why is Letter of Credit important?

A letter of credit is beneficial for both the parties as it assures the seller that he will receive his funds upon fulfillment of terms of the trade agreement and the buyer can portray his creditworthiness and negotiate longer payment terms, by having a bank back the trade transaction.

Features / Characteristics of letter of credit

A letter of credit is identified by certain principles. These principles remain the same for all kinds of letters of credit. The main characteristics of letters of credit are as follows:

Negotiability

A letter of credit is a transactional deal, under which the terms can be modified/changed at the parties assent. In order to be negotiable, a letter of credit should include an unconditional promise of payment upon demand or at a particular point in time.

Revocability

A letter of credit can be revocable or irrevocable. Since a revocable letter of credit cannot be confirmed, the duty to pay can be revoked at any point of time. In an irrevocable letter of credit, all the parties hold power, it cannot be changed/modified without the agreed consent of all the people.

Transfer and Assignment

A letter of credit can be transferred, also the beneficiary has the right to transfer/assign the LC. The LC will remain effective no matter how many times the beneficiary assigns/transfers the LC.

Sight & Time Drafts

The beneficiary will only receive the payment upon maturity of letter of credit from the issuing bank when he presents all the drafts & the necessary documents.

Documents required for a Letter of Credit

- Shipping Bill of Lading

- Airway Bill

- Commercial Invoice

- Insurance Certificate

- Certificate of Origin

- Packing List

- Certificate of Inspection

How does Letter of Credit Work?

LC is an arrangement whereby the issuing bank can act on the request and instruction of the applicant (importer) or on their own behalf. Under an LC arrangement, the issuing bank can make a payment to (or to the order of) the beneficiary (that is, the exporter). Alternatively, the issuing bank can accept the bills of exchange or draft that are drawn by the exporter. The issuing bank can also authorize advising or nominated banks to pay or accept bills of exchange.

Fee and charges payable for an LC

There are various fees and reimbursements involved when it comes to LC. In most cases, the payment under the letter of credit is managed by all parties. The fees charged by banks may include:

Opening charges, including the commitment fees, charged upfront, and the usance fee that is charged for the agreed tenure of the LC.

Retirement charges are payable at the end of the LC period. They include an advising fee charged by the advising bank, reimbursements payable by the applicant to the bank against foreign law-related obligations, the confirming bank’s fee, and bank charges payable to the issuing bank.

Parties involved in an LC

Main parties involved:

Applicant An applicant (buyer) is a person who requests his bank to issue a letter of credit.

Beneficiary A beneficiary is basically the seller who receives his payment under the process.

Issuing bank The issuing bank (also called an opening bank) is responsible for issuing the letter of credit at the request of the buyer.

Advising bank The advising bank is responsible for the transfer of documents to the issuing bank on behalf of the exporter and is generally located in the country of the exporter.

Other parties involved in an LC arrangement:

Confirming bank The confirming bank provides an additional guarantee to the undertaking of the issuing bank. It comes into the picture when the exporter is not satisfied with the assurance of the issuing bank.

Negotiating bank The negotiating bank negotiates the documents related to the LC submitted by the exporter. It makes payments to the exporter, subject to the completeness of the documents, and claims reimbursement under the credit.

(Note:- Negotiating bank can either be a separate bank or an advising bank)

Reimbursing bank The reimbursing bank is where the paying account is set up by the issuing bank. The reimbursing bank honors the claim that settles the negotiation/acceptance/payment coming in through the negotiating bank.

Second Beneficiary The second beneficiary is one who can represent the original beneficiary in their absence. In such an eventuality, the exporter’s credit gets transferred to the second beneficiary, subject to the terms of the transfer.

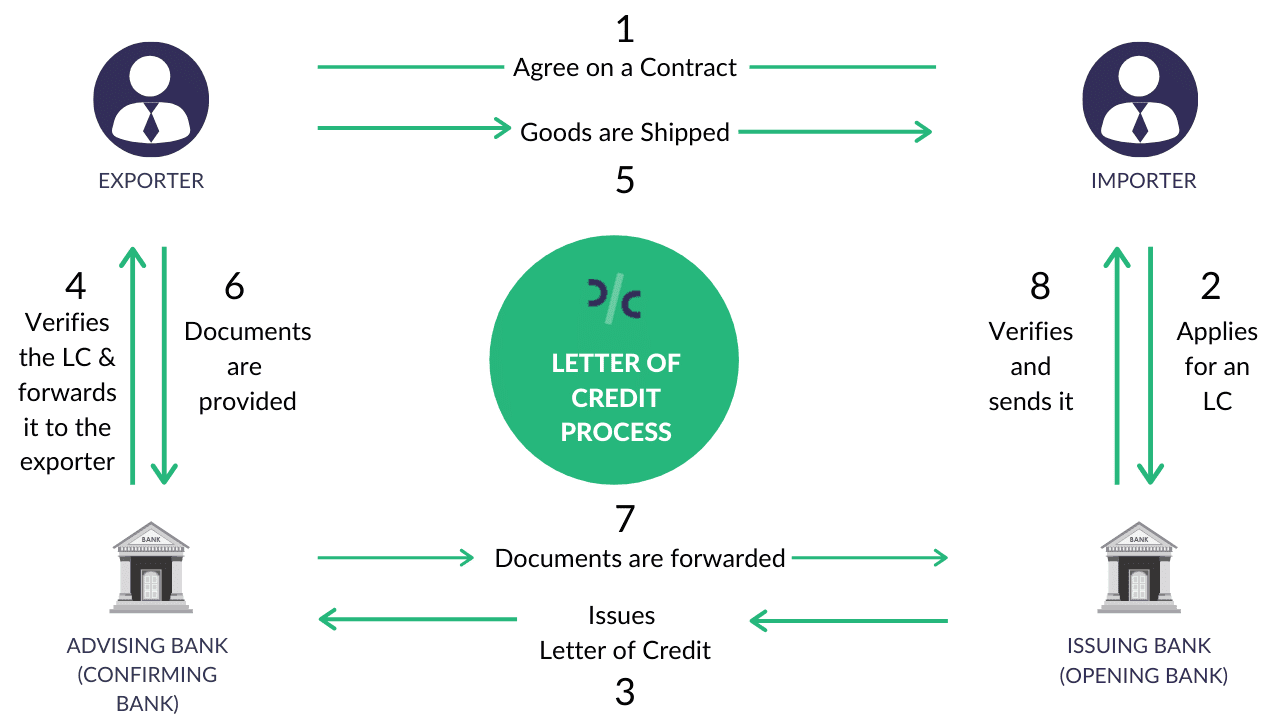

What is the process of getting an LC?

The process of getting an LC consists of four primary steps, which are enlisted here:

Step 1 - Issuance of LC

After the parties to the trade agree on the contract and the use of LC, the importer applies to the issuing bank to issue an LC in favor of the exporter. The LC is sent by the issuing bank to the advising bank. The latter is generally based in the exporter’s country and may even be the exporter’s bank. The advising bank (confirming bank) verifies the authenticity of the LC and forwards it to the exporter.

Step 2 - Shipping of goods

After receipt of the LC, the exporter is expected to verify the same to their satisfaction and initiate the goods shipping process.

Step 3 - Providing Documents to the confirming bank

After the goods are shipped, the exporter (either on their own or through the freight forwarders) presents the documents to the advising/confirming bank.

Step 4 - Settlement of payment from importer and possession of goods

The bank, in turn, sends them to the issuing bank and the amount is paid, accepted, or negotiated, as the case may be. The issuing bank verifies the documents and obtains payment from the importer. It sends the documents to the importer, who uses them to get possession of the shipped goods.

What is an example of an LC?

Suppose Mr. A (an India based exporter) has a sales contract with Mr. B (an importer from Australia) for delivering a batch of medical equipment to the latter. Both parties being unknown to each other, decide to go for an LC arrangement. Company B applies for a letter of credit with a bank in Australia. The document assures Mr. A of the payment in exchange for the shipment of the cargo. From this point on, this is how a letter of credit transaction would unveil between Mr. A & Mr. B:-

- Mr. B (buyer) goes to their bank, that is, the issuing bank or opening bank, and requests to issue an LC.

- The issuing bank further processes the LC to the advising bank (A's India-based bank).

- The advising bank checks the authenticity of the LC and sends it to Mr. A.

- Now Mr. A will ship the goods.

- Furthermore, they will send specific trade documents, including the bill of lading, to the negotiating bank.

- The negotiating bank will make sure that all requirements are fulfilled and make the payment to Mr. A.

- Additionally, the negotiating bank will send all the necessary documents, including the bill of lading, to the issuing bank.

- The issuing bank will send these documents to Mr. B (Buyer) to confirm their authenticity.

- After the confirmation of shipment, Company B completes the payment to Company A in India.

- And the issuing bank will pass on the funds to the negotiating bank.

- If Company B is not able to furnish the required funds, their issuing bank completes payment on their behalf.

To understand the process clearly refer to this image:

Letter of credit Sample Format

Types of Letter of Credit

Following are the most commonly used or known types of letter of credit:-

- Revocable Letter of Credit

- Irrevocable Letter of Credit

- Confirmed Letter of Credit

- Unconfirmed Letter of Credit

- LC at Sight

- Usance LC or Deferred Payment LC

- Back to Back LC

- Transferable Letter of Credit

- Un-transferable Letter of Credit

- Standby Letter of Credit

- Freely Negotiable Letter of Credit

- Revolving Letter of Credit

- Red Clause LC

- Green Clause LC

To understand each type in detail read the article, Types of letter of credit used in International Trade.

What is the application process for an LC?

Importers have to follow a specific procedure to follow for the application of LCs. The process is listed here:

- After a sales agreement is created and signed between the importer and the exporter, the importer applies to their bank to draft a letter of credit in favor of the exporter.

- The issuing bank (importer’s bank) creates a letter of credit that matches the terms and conditions of the sales agreement before sending it to the exporter’s bank.

- The exporter and their bank need to evaluate the creditworthiness of the issuing bank. After doing so and verifying the letter of credit, the exporter’s bank approves and sends the document to the importer.

- After that, the exporter manufactures and ships the goods as per the agreed timeline. A shipping line or freight forwarder assists with the delivery of goods.

- Along with the goods, the exporter also submits documents to their bank for compliance with the sales agreement.

- After approval, the exporter’s bank then sends these complying documents to the issuing bank.

- Once the documents are reviewed, the issuing bank releases the payment to the exporter and sends the documents to the importer to collect the shipment.

What are the Benefits of an LC?

A letter of credit is beneficial for both parties as it assures the seller that they will receive their funds upon fulfillment of the terms of the trade agreement, while the buyer can portray his creditworthiness and negotiate longer payment terms by having a bank back the trade transaction.

Letters of credit have several benefits for both the importer and the exporter. The primary benefit for the importer is being able to control their cash flow by avoiding prepayment for goods. Meanwhile, the chief advantage for exporters is a reduction in manufacturing risk and credit risk. Ultimately, since the trade deals are often international, there are factors like location, distance, laws, and regulations of the involved countries that need to be taken into account. The following are advantages of a letter of credit explained in detail.

LC reduces the risk of late-paying or non-paying importers There might be instances when the importer changes or cancels their order while the exporter has already manufactured and shipped the goods. The importers could also refuse payment for the delivered shipments due to a complaint about the goods. In such circumstances, a letter of credit will ensure that the exporter or seller of the goods receives their payment from the issuing bank. This document also safeguards if the importer goes into bankruptcy.

LC helps importers prove their creditworthiness Small to midsize businesses do not have vast reserves of capital for managing payments for raw materials, equipment, or any other supplies. When they are in a contract to manufacture a product and send it to their client within a small window, they cannot wait around to free up capital for buying supplies. This is where letters of credit come to their rescue. A letter of credit helps them with important purchases and serves as proof to the exporter that they will fulfill the payment obligations, thus avoiding any transaction and manufacturing delays.

LCs help exporters with managing their cash flow more efficiently A letter of credit also ensures that payment is received on time for the exporters or sellers. This is especially important if there is a huge period of time between the delivery of goods and payment for them. Ensuring timely payments through the letter of credit will go a long way in helping the exporters manage their cash flow. Furthermore, sellers can obtain financing between the shipment of goods and receipt of payment, which can provide an additional cash boost in the short term.

Bank guarantee vs letter of credit

A Bank guarantee is a commercial instrument. It is an assurance given by the bank for a non-performing activity. If any activity fails, the bank guarantees to pay the dues. There are 3 parties involved in the bank guarantee process i.e the applicant, the beneficiary and the banker.

Whereas, a Letter of Credit is a commitment document. It is an assurance given by the bank or any other financial institution for a performing activity. It guarantees that the payment will be made by the importer subjected to conditions mentioned in the LC. There are 4 parties involved in the letter of credit i.e the exporter, the importer, issuing bank and the advising bank (confirming bank).

Things to consider before getting an LC

A key point that exporters need to remind themselves of is the need to submit documents in strict compliance with the terms and conditions of the LC. Any sort of non-adherence with the LC can lead to non-payment or delay and disputes in payment.

The issuing bank should be a bank of robust reputation and have the strength and stability to honor the LC when required.

Another point that must be clarified before availing of an LC is to settle the responsibility of cost-bearing. Allotting costs to the exporter will escalate the cost of recovery. The cost of an LC is often more than that of other modes of export payment. So, apart from the allotment of costs, the cost-benefit of an LC compared to other options must also be considered.

FAQs on Letter of Credit

1. Is Letter of Credit safe?

Yes. Letter of Credit is a safe mode of payment widely used for international trade transactions.

2. How much does it cost for a letter of credit?

Letters of credit normally cost 1% of the amount covered in the contract. But the cost may vary from 0.25% to 2% depending on various other factors.

3. Can a letter of credit be cancelled?

In most cases letters of credit are irrevocable and cannot be cancelled without the agreed consent of all parties.

4. Can a letter of credit be discounted?

A letter of credit can be discounted. While getting an LC discounted the supplier or holde of LC should verify whether the issuing bank is on the approved list of banks, with the discounting bank. Once the LC is approved, the discounting bank releases the funds after charging a certain amount as premium.

5. Is a letter of credit a not negotiable instrument?

A letter of credit is said to be a negotiable instrument, as the bank has dealings with the documents and not the goods the transaction can be transferred with the assent of the parties.

6. Are letters of credit contingent liability?

It would totally depend on future circumstances. For instance, if a buyer is not in a condition to make the payment to the bank then the bank has to bear the cost and make the arrangement on behalf of the buyer.

7. A letter of credit is with recourse or without recourse?

A 'without recourse' letter of credit to the beneficiary is a confirmed LC. Whereas an unconfirmed or negotiable letter of credit is 'with recourse' to the beneficiary.

8. Who is responsible for letters of credit?

The issuing bank takes up the responsibility to complete the payment if the importer fails to do so. If it is a confirmed letter of credit, then the confirming bank has the responsibility to ensure payment if the issuing bank and importers fail to make the payment.

The Uniform Customs and Practice for Documentary Credits (UCP) describes the legal framework for all letters of credit. The current version is UCP600 which stipulates that all letters will be irrevocable until specified.

Also Read: